Credit scores are numerical representations of your creditworthiness, typically ranging from 300 to 850. They’re calculated based on various factors that lenders use to assess the risk of lending you money. Before diving into loan options, it’s essential to understand what constitutes your credit score:

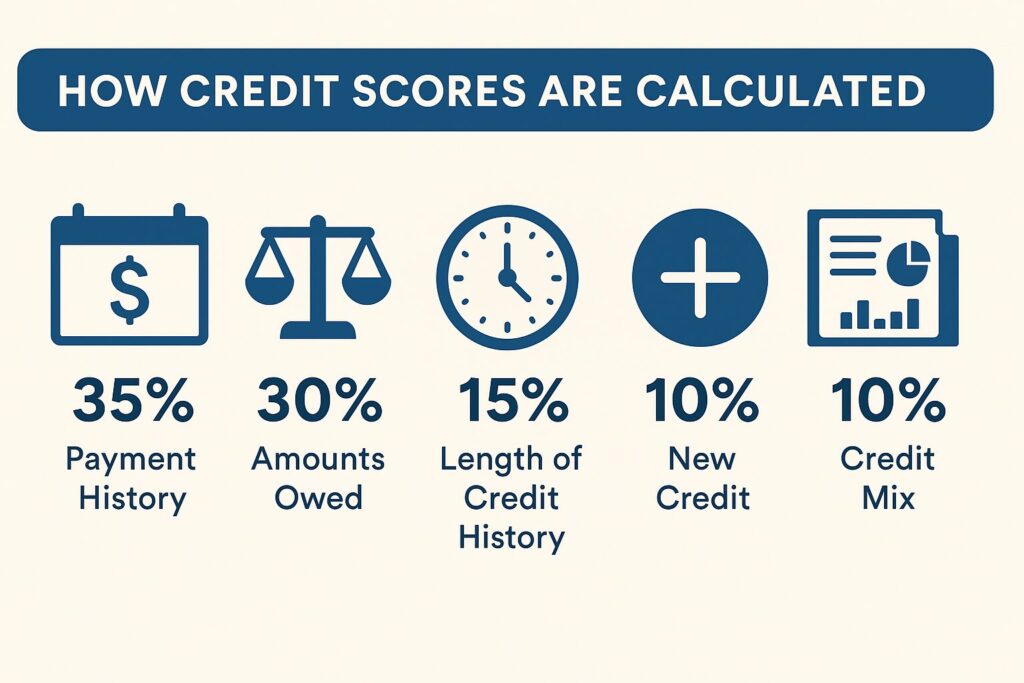

How Credit Scores Are Calculated

- Payment History (35%): Your track record of paying bills on time is the most significant factor in your credit score calculation. Late payments, collections, and bankruptcies can significantly damage this component.

- Credit Utilization / Amounts Owed (30%): This represents how much of your available credit you’re using. Experts recommend keeping this ratio below 30% for optimal credit health.

- Length of Credit History (15%): The age of your oldest account, the average age of all accounts, and how recently you’ve used certain accounts all factor in here.

- Credit Mix (10%): Having various types of credit (credit cards, installment loans, retail accounts) demonstrates your ability to manage different financial obligations.

- New Credit Inquiries (10%): Each time you apply for new credit, a hard inquiry appears on your report, which can temporarily lower your score.

What Constitutes “Fair Credit”

A fair credit score typically falls between 580 and 669 on the FICO scale. This range indicates to lenders that while you’ve had some challenges with credit in the past, you’re still a viable candidate for loans—albeit at potentially higher interest rates than those with excellent credit.Step-by-Step Preparation Before Applying

1. Check Your Credit Reports and Scores

Action steps:

- Request free reports from all three bureaus (Experian, Equifax, TransUnion) through AnnualCreditReport.com

- Review for errors or discrepancies that could be lowering your score

- Dispute any inaccuracies by writing to the credit bureaus with supporting documentation

- Use credit monitoring services or apps that offer free score access

- Note that your FICO score may differ from educational scores provided by free services

2. Assess Your Current Financial Situation

Action steps:

- Calculate your debt-to-income (DTI) ratio by dividing your monthly debt payments by your gross monthly income

- Aim for a DTI below 43%, as this is often the maximum acceptable ratio for many lenders

- Create a detailed list of all existing debts and monthly obligations

- Determine exactly how much you need to borrow and why

- Calculate how much you can realistically afford to repay monthly

3. Improve Your Credit Before Applying

Action steps:

- Pay down credit card balances to reduce utilization

- Set up automatic payments for all bills to ensure timeliness

- Avoid applying for new credit cards or loans in the months before your loan application

- If possible, become an authorized user on a family member’s long-standing, well-managed credit account

- Consider using tools like Experian Boost to get credit for utility and subscription payments

4. Gather Required Documentation

Action steps:

- Collect recent pay stubs (last 2-3 months)

- Prepare your last two years of tax returns

- Have bank statements ready (typically last 2-3 months)

- Make a list of all addresses from the past 2-5 years

- Prepare employment history information for the past 2 years

- Have government-issued ID ready

Finding and Comparing Suitable Lenders

1. Research Different Lender Types

Online Lenders

- Pros: Often have more flexible requirements, faster processing, and convenience

- Cons: May charge higher rates or fees

- Examples: LendingPoint, Upstart, OneMain Financial

- Best for: Quick funding and convenience

Credit Unions

- Pros: Often offer lower rates (federal credit unions cap rates at 18%), more personalized service

- Cons: May require membership

- Best for: Potentially lower rates and relationship-based lending

Community Banks

- Pros: May consider factors beyond your credit score

- Cons: Might have limited loan products

- Best for: Existing customers and those who value relationship banking

Peer-to-Peer Platforms

- Pros: Alternative approval criteria that might work in your favor

- Cons: Can have higher origination fees

- Best for: Those with unique financial situations that traditional lenders might reject

2. Utilize Pre-qualification Tools

Action steps:

- Use lenders’ pre-qualification tools that perform soft credit checks

- Compare at least 3-5 different offers side by side

- Look beyond the interest rate to understand the full offer

- Document each pre-qualification result for comparison

3. Analyze Loan Offers Comprehensively

Create a comparison spreadsheet with these columns:

- Lender name

- Pre-qualified loan amount

- Interest rate/APR

- Loan term options

- Monthly payment amount

- Origination fee (amount and percentage)

- Late payment fees

- Prepayment penalties

- Funding time

- Customer service ratings

Understanding Loan Terms and Features

1. Interest Rates vs. APR

What to know:

- Interest rate represents the cost of borrowing the principal

- APR includes both interest rate and fees, providing a more comprehensive view of cost

- Example: A loan with 12% interest rate plus a 4% origination fee has an APR closer to 16%

2. Fixed vs. Variable Rates

What to consider:

- Fixed rates remain constant throughout the loan term

- Variable rates may start lower but can increase based on market conditions

- For fair credit borrowers, fixed rates provide predictability and protection against potential rate increases

3. Term Length Considerations

How to decide:

- Shorter terms (12-36 months): Higher monthly payments but less interest paid overall

- Longer terms (48-60+ months): Lower monthly payments but significantly more interest over time

- Calculate the total cost difference between term options before deciding

Example calculation for a $10,000 loan at 15% interest:

- 3-year term: $347/month, $2,492 total interest

- 5-year term: $237/month, $4,220 total interest

- Difference: $1,728 more in interest for the longer term

4. Understanding Fees

Critical fees to identify:

- Origination fees: Typically 1-12% of the loan amount, often deducted from loan proceeds

- Application fees: One-time charges for processing your application

- Late payment fees: Usually either a percentage of payment or flat fee ($15-$40)

- Prepayment penalties: Charges for paying off the loan early (avoid lenders with these if possible)

- NSF/returned payment fees: Charges for insufficient funds ($25-$40 per occurrence)

The Application Process

1. Preparing Your Application

Action steps:

- Double-check all information for accuracy

- Be truthful about income and expenses (falsifying information can lead to loan denial or legal issues)

- Prepare explanations for any negative items on your credit report

- Consider writing a brief letter explaining any extenuating circumstances that affected your credit

2. Choosing the Right Time to Apply

Strategic timing:

- Apply when your credit utilization is lowest (ideally after paying down credit cards)

- Avoid applying soon after other credit applications

- Consider applying early in the week to avoid processing delays that might occur on weekends

3. The Application Submission

Best practices:

- Complete applications within the same 14-day period to minimize credit score impact

- Save or print confirmation pages and application numbers

- Follow up within 2-3 business days if you haven’t heard back

- Be prepared to provide additional documentation quickly if requested

4. Dealing with Approval, Conditional Approval, or Denial

If approved:

- Review the final terms carefully before accepting

- Confirm there are no changes from the pre-qualified offer

- Set up autopay to ensure on-time payments

If conditionally approved:

- Provide any additional documentation promptly

- Ask for clarification on any conditions you don’t understand

- Consider negotiating terms if they differ significantly from what was expected

If denied:

- Request the specific reason for denial

- Ask if there are steps you can take to qualify in the future

- Consider a secured loan or adding a co-signer if appropriate

- Wait at least 3-6 months before reapplying to the same lender

Alternative Options When Traditional Loans Aren’t Available

1. Secured Personal Loans

How they work:

- Require collateral (savings account, CD, vehicle)

- Typically offer lower interest rates

- Represent less risk to lenders, increasing approval odds

- Usually have faster approval processes

2. Co-signer Options

Important considerations:

- Co-signer must have good-to-excellent credit

- Both parties are equally responsible for repayment

- Late payments affect both credit scores

- Have a written agreement detailing responsibilities

- Some lenders allow co-signer release after a period of on-time payments

3. Credit Builder Products

Options to consider:

- Credit-builder loans from credit unions

- Secured credit cards to establish payment history

- Self-credit builder accounts that combine savings with credit building

Managing Your Loan Successfully

1. Setting Up Payment Systems

Best practices:

- Enroll in autopay (some lenders offer rate discounts for this)

- Set payment dates shortly after your regular payday

- Create calendar reminders as backups

- Maintain a buffer amount in your payment account

2. Monitoring Your Credit Progress

Action steps:

- Check your credit score monthly to track improvements

- Review how the loan is reported to credit bureaus

- Address any reporting errors immediately

- Document all payments made and confirmations received

3. Strategies for Paying Off Early

Approaches to consider:

- Round up payments to the nearest $50 or $100

- Make bi-weekly instead of monthly payments

- Apply any windfalls (tax refunds, bonuses) to the principal

- Check if your lender applies extra payments to principal automatically

4. When to Consider Refinancing

Indicators it’s time to refinance:

- Your credit score has improved by 50+ points

- Interest rates have dropped significantly

- Your income has increased substantially

- You want to change your monthly payment amount

- Wait at least 6-12 months of on-time payments before attempting to refinance

Common Pitfalls and How to Avoid Them

1. Predatory Lending Warning Signs

Red flags to watch for:

- Interest rates above 36% APR

- Pressure to borrow more than requested

- Excessive fees (origination fees over 8%)

- No credit check required

- Guarantees of approval before reviewing your information

- Requests for upfront fees before loan approval

2. Avoiding Debt Cycles

Preventive strategies:

- Only borrow what you absolutely need

- Have a clear repayment plan before accepting funds

- Avoid using new loans to pay off existing debts unless the terms are significantly better

- Create an emergency fund to avoid future borrowing needs

3. Protecting Your Personal Information

Security measures:

- Verify lender legitimacy through the Better Business Bureau and NMLS Consumer Access

- Never provide financial information on unsecured websites

- Be suspicious of lenders contacting you through social media or cold calls

- Check for secure connection (https://) before entering personal data

- Read privacy policies regarding how your information will be used

Conclusion: Building Toward Better Credit

Personal loans with fair credit can be stepping stones to improved financial health when managed properly. By understanding the loan landscape, carefully comparing options, and maintaining impeccable payment discipline, you can use this experience to demonstrate creditworthiness and gradually qualify for better terms in the future.

Remember that each on-time payment builds your credit history positively. With disciplined management of your personal loan, you can expect to see credit score improvements within 6-12 months, potentially opening doors to more favorable financial products in the future.