In a perfect world, every loan application would be approved instantly — no credit checks, no income verification, just money when you need it. But in the real world? “Guaranteed approval” is usually a red flag, not a feature.

That doesn’t mean you’re out of options if your credit is shaky or you’ve been denied in the past. The key is understanding what “everyone-approved” really means — and where you can find legitimate lenders that work with low credit scores, limited credit histories, or inconsistent income.

This guide breaks down the types of loans most accessible to people with limited options, who they work best for, and how to protect yourself while still getting the money you need.

What “Everyone-Approved” Really Means

Let’s be clear: no reputable lender guarantees approval for everyone without condition. If someone promises a loan with:

- No credit check

- No income verification

- Instant deposit

…that’s often code for high-interest payday loans or scam operations.

Legitimate lenders do offer high-approval-rate loans, but they still have basic checks in place — they just tend to be more flexible about who qualifies.

Key traits of accessible, real loans:

- Accept low or fair credit scores (typically 560+)

- Offer secured options (using collateral)

- Allow co-signers

- Use cash flow or banking history instead of credit

Best Loan Types with High Approval Rates

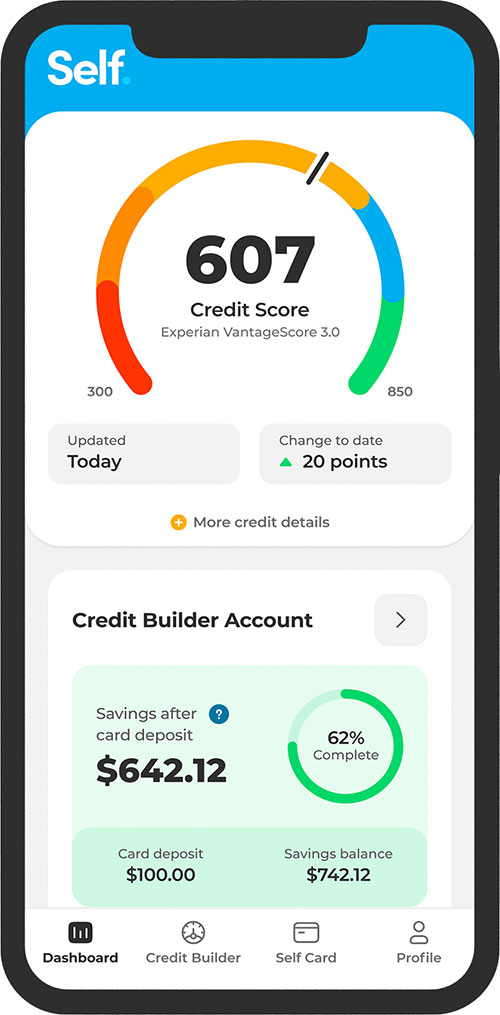

Credit Builder Loans

Best for: People with no credit or very poor credit who want to establish history while saving money

How they work:

You don’t get the money up front. Instead, you make monthly payments into a locked savings account. Once it’s paid off, you receive the full amount — and your on-time payments are reported to credit bureaus.

Why it matters:

It’s one of the rare products that both improves your credit and helps you build a small nest egg. You’re essentially “borrowing from yourself” — and proving your creditworthiness in the process.

Secured Personal Loans

Best for: Borrowers with bad credit who own a car, savings account, or other asset

Loan features:

- You use collateral (like a car title or savings account) to secure the loan

- Lower interest rates than unsecured loans

- Higher approval chances, even with credit below 600

How you benefit:

Lenders are more willing to approve riskier borrowers when there’s an asset on the line. This lets you access better loan terms even with a low score — but defaulting means losing your collateral.

Peer-to-Peer (P2P) Loans

Best for: Borrowers with fair credit and steady income who want to avoid banks

Popular platforms: LendingClub, Prosper, Upstart

This is why it works:

Unlike traditional banks, P2P lenders match you with individual investors. Many use alternative underwriting like job history or education level instead of relying only on your credit score.

- Approval possible with credit as low as 580–600

- Loan amounts: $1,000–$40,000

- Rates typically range from 7%–36%

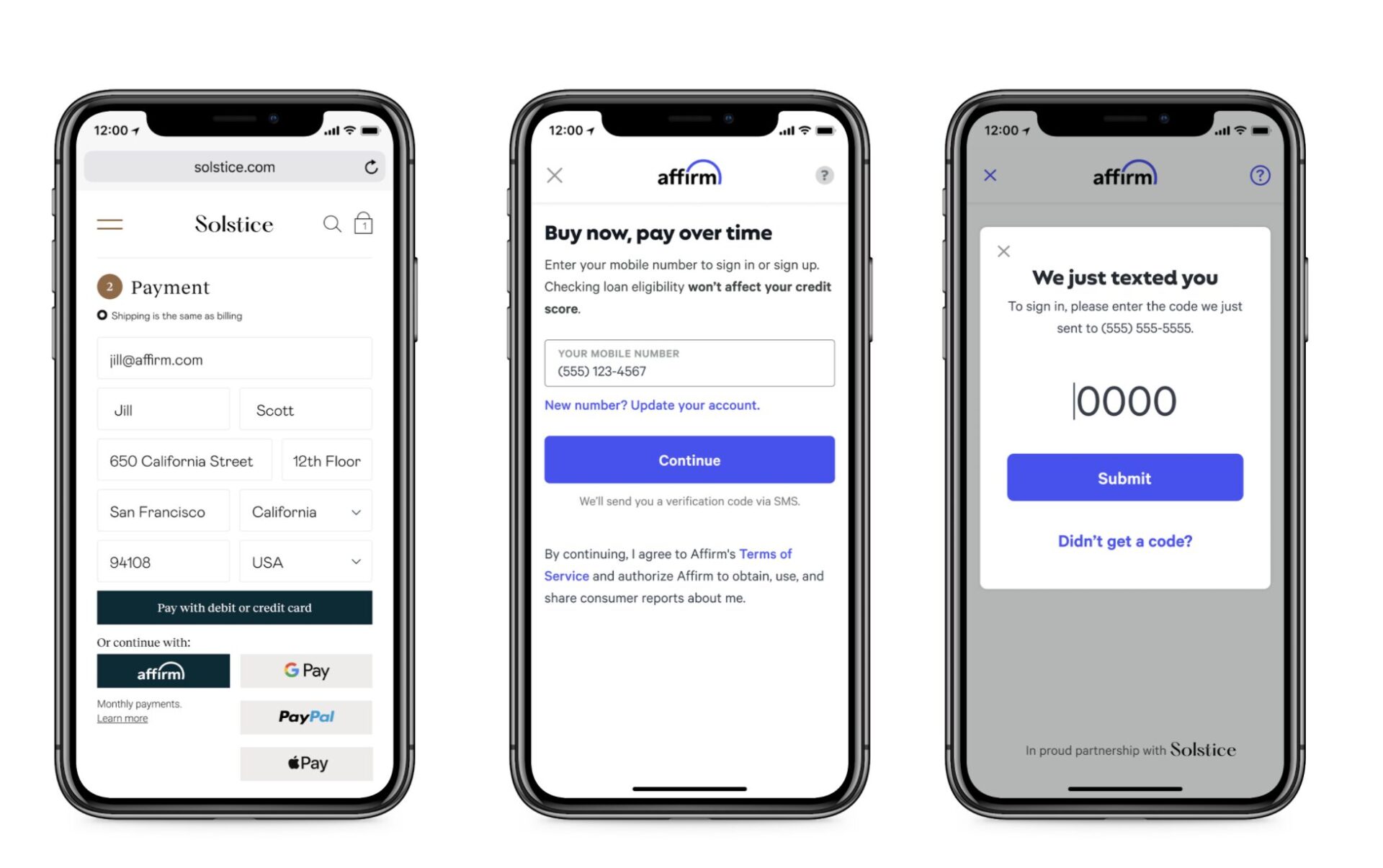

Buy Now, Pay Later (BNPL) Loans

Best for: Small purchases under $1,000 — like electronics, furniture, or emergency needs

Common providers: Affirm, Klarna, Afterpay

How you’ll notice the perks:

There’s usually no hard credit check, and approval rates are extremely high — especially for lower amounts and repeat customers. Payments are broken into 4–6 monthly installments, often interest-free.

Caution:

Missed payments can still impact your credit or lead to collections, even if the lender didn’t check your credit to begin with.

Personal Loans from Credit Unions

Best for: Members of local or online credit unions with limited borrowing history

Why they’re different:

Credit unions are member-owned and often more willing to work with low-credit borrowers. Some even offer payday alternative loans (PALs), which cap interest at 28% and are designed to be safe options for emergency funds.

Example:

PenFed and Navy Federal both offer small personal loans starting around $600, often with flexible terms and fast approval if you’re a member.

Payday Alternative Loans (PALs)

Best for: People facing short-term cash emergencies who want to avoid payday lenders

How it works:

Offered only by federal credit unions, these loans:

- Are capped at $2,000

- Have interest rates limited to 28%

- Come with repayment terms of up to 12 months

- Require at least one month of credit union membership

This is why it matters:

It’s the only short-term loan category designed specifically as a safe alternative to predatory payday loans. No rollovers, no 400% APR, and no trap doors.

Loan Types to Avoid

Some loan types come with near-certain approval — but at a serious cost. These should be used only when you’ve exhausted all other options.

Payday Loans:

- Approval in minutes, but APR often exceeds 400%

- Repayment terms usually two weeks — setting up a debt trap

Auto Title Loans:

- Use your car as collateral, but failure to repay can result in immediate repossession

No-Credit-Check Installment Loans (from unlicensed lenders):

- Common online scam target — fees buried in fine print, sky-high rates

If it sounds too easy, read the fine print twice.

Comparison Table: Accessible Loan Options

| Loan Type | Credit Needed | Typical Amount | Approval Speed | Risk Level | Interest Range |

|---|---|---|---|---|---|

| Credit Builder Loans | No credit | $300–$1,000 | 1–3 days | Low | ~10%–15% |

| Secured Personal Loans | Poor/Fair | $1,000–$50,000 | 1–3 days | Medium | ~6%–25% |

| Peer-to-Peer Loans | 580+ | $1,000–$40,000 | 1–5 days | Medium | ~7%–36% |

| BNPL Loans | Very low | $50–$2,000 | Instant–1 day | Low–Medium | 0%–30% |

| Credit Union Personal Loans | Poor/Fair | $600–$15,000 | 1–2 days | Low | ~8%–18% |

| Payday Alternative Loans | Any | $200–$2,000 | 1–2 days | Low | ≤28% |

Final Thought: Approval Isn’t Everything

High-approval loans can be a lifeline — but they’re not all created equal. Focus on:

- Terms you can afford

- Lenders with transparency

- Products that build, not break, your financial future

Look past the ads promising “guaranteed approval” and start with options that are both accessible and sustainable. If your score is below 600, start with credit unions, secured loans, or credit builders. If you’re above that, peer-to-peer and BNPL options can be useful tools — when used responsibly.